Duration 10:14

Option vega (FRM T4-17)

Published 28 Feb 2019

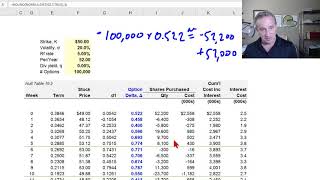

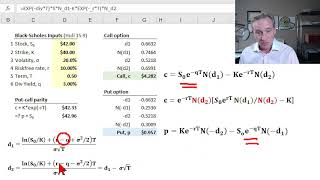

[my xls is here https://trtl.bz/2T7KDtG] Vega is the sensitivity of an option's value to volatility. Vega tends to be highest when the option is at-the-money (ATM). In this example, where S = K = 100, σ = 30%, T = 1.0 year, and Rf = 4.0%, the vega is 38.32. This is the (linearly estimated) change in the option value per one unit (ie, 100%) change in volatility. Therefore, this vega predicts a change of +$0.38 if the volatility increases by +1.0% to 39.0%. In this way, by convention, we could divide the 38.32 by 100 = $0.3832 to express vega as the dollar change per PERCENTAGE POINT change in volatility. Discuss this video here in our FRM forum: https://trtl.bz/30AWCAb

Category

Show more

Comments - 17

Related videos for Option vega (FRM T4-17):